With Asian stocks retreating on worrying data from China and some consumer diffidence in the holiday season, the emerging market currencies are bound to be under pressure as the flight to dollar strengthens. Markets seem to be worried at the Chinese slow down. The Indian Rupee also is likely to be under pressure as a natural consequence and aided also by the relaxation in import curbs.The Indian stock market will be influenced by the retreat in Asian stocks. Moreover with the Governor of the Reserve Bank of India unlikely to reduce interest rates any soon, despite the pleas of the Finance Minister, the corporate sector has nothing to display forth at this moment. The economic fraternity has also take concerns expressed by the Governor on the scale of NPA in the banking sector. There are qualitative issues too. Overall a day where sellers may outnumber.

Sunday, November 30, 2014

Gold and oil

Both seem set south. With the crash in oil prices, fears of deflation run the roost. That means the utility of gold as a hedging deployment is very limited. Given the industrial demand is sluggish, gold cannot be on an upward move immediately. China is slowed and India looks slowing as per latest Gdp , so the outlook for gold from these 2 main buyers is not too encouraging in the short run. The Swiss have just rejected any plans for its central bank to buy more gold. That should add to seller list.

Success of the USA geo economic Strategy

The increased production of shale oil seems to break the back of OPEC. In a few weeks, the price of oil has dropped dramatically, diving from $100 now to $ 70. This has led the Saudis struggling to protect a market share and adopt a cut price strategy which would have to be followed by others.

Strategically it is a great time for the Americans as the current scenario shows:

a) the weakness of OPEC;

b) GCC countries will now be struggling to meet their budget targets;

c) Russia is further weakened;

d) newly emerging oil countries like Libya, Iraq and Iran can no more play the money power houses that they once were.

Geo political strategy led by geo economics.

Strategically it is a great time for the Americans as the current scenario shows:

a) the weakness of OPEC;

b) GCC countries will now be struggling to meet their budget targets;

c) Russia is further weakened;

d) newly emerging oil countries like Libya, Iraq and Iran can no more play the money power houses that they once were.

Geo political strategy led by geo economics.

Egypt : Winter of Arab Spring 2011

2011 Arab Spring saw Tahrir Square overthrow Mubarak. Egyptians celebrated as he fell in disgrace. However, immature democracy that Egypt is it sank into near anarchy. Tourists , Egypt's mainstay revenue givers, stopped coming. Egypt's pound has since slipped and slipped miserably dollar to Egyptian pound at 5.8 in 2011 to 7.10 official; (7,50 in black ) There is a black market which is nearly 8 % behind the official rate. With the dollar rising, that spread will widen in favour of those who have dollars. Inflation exceeded 11.5 % last year. IMF estimates estimates

that the budget deficit will reach about 11 percent of GDP,

With oil prices falling and the benefactors in GCC not seeing a power anymore in Egypt, this country seems slipping and slipping. Holding on to Egyptian assets seems a decline in wealth.

Egypt’s

foreign reserves, which stood at $36bn on the eve of the Revolution,

currently hovers around 3 months imports at $13.

Thursday, November 27, 2014

OPEC does not cut production

Its 30 million barrels to stay. Good for input costs. Bad news for Russia, Norway, GCC, Iran. Libya, Iraq, Indonesia.

"the success of monetary union anywhere depends on its success everywhere."

Mario Draghi: Stability and prosperity in Monetary Union

Speech by Mr Mario Draghi, President of the European Central Bank, at the University of Helsinki, Helsinki,

Sovereign debt needs also to act as a safe haven in times of economic stress. It can do so first of all through a strong fiscal governance framework. Secondly, by having some form of backstop for sovereign debt in place. "Over the longer-term", "it would be natural to reflect further on whether we have done enough in the euro area to preserve at all times the ability to use fiscal policy counter-cyclically. But it is also clear that- this could only take place in the context of a decisive step towards closer Fiscal Union".

http://www.bis.org/review/r141127i.htm

Economic Impact of Ebola from World Bank

World Bank on costs of Ebola

" The short-term (2014) impact on output, estimated using on-the ground data to inform revisions to sector-specific growth projections, is in the order of 2.1 percentage points (pp) of gross domestic product (GDP) in Guinea (reducing growth from 4.5 percent to 2.4 percent); 3.4 pp of GDP in Liberia (reducing growth from 5.9 percent to 2.5 percent) and 3.3 pp of GDP in Sierra Leone (reducing growth from 11.3 percent to 8.0 percent). This forgone output for these three countries corresponds to US$359 million in 2013 prices.

• The short-term fiscal impacts are also large, at US$113 million (5.1 percent of GDP) for Liberia; US$95 million (2.1 percent of GDP for Sierra Leone) and US$120 million (1.8 percent of GDP) for Guinea. These estimates are best viewed as lower-bounds. "

https://openknowledge.worldbank.org/bitstream/handle/10986/20592/9781464804380.pdf?sequence=5

" The short-term (2014) impact on output, estimated using on-the ground data to inform revisions to sector-specific growth projections, is in the order of 2.1 percentage points (pp) of gross domestic product (GDP) in Guinea (reducing growth from 4.5 percent to 2.4 percent); 3.4 pp of GDP in Liberia (reducing growth from 5.9 percent to 2.5 percent) and 3.3 pp of GDP in Sierra Leone (reducing growth from 11.3 percent to 8.0 percent). This forgone output for these three countries corresponds to US$359 million in 2013 prices.

• The short-term fiscal impacts are also large, at US$113 million (5.1 percent of GDP) for Liberia; US$95 million (2.1 percent of GDP for Sierra Leone) and US$120 million (1.8 percent of GDP) for Guinea. These estimates are best viewed as lower-bounds. "

https://openknowledge.worldbank.org/bitstream/handle/10986/20592/9781464804380.pdf?sequence=5

London losing steam as a financial centre?

For decades, London, with its time zone positioning had a natural advantage as the World's largest volume driven financial centre. New York and Tokyo followed tamely for years. Thatcher's big bang helped re-inforce the London Lead. So much so that London became a centre for Islamic Finance too!

With the rise of Asia and the innovativeness of the Americans and the tottering of Europe, things have changed. The Chinese have post Kissinger days, been more at home in USA than than in imperial England. Chinese students go by hordes to USA. The rich Arabs have diversified to continental Europe from France to Germany to Spain. London's key banks have also been affected by recession woes and LIBOR fixing scandals and even probable legal violations (in USA) . The Pound is no more an alternative currency, forget a safe haven. Cable (GBP/Dollar) is virtually history.

With the growth of Dubai, Arab funds might see a return nearer home; with Singapore's proximity to China ; with ECB in Frankfurt, with the colonies no more to fund regal splendour; with its universities badly behind in revenues and perhaps research, with Scottish threats, imperious London's real estate and real finances may soon be under pressure.

With the rise of Asia and the innovativeness of the Americans and the tottering of Europe, things have changed. The Chinese have post Kissinger days, been more at home in USA than than in imperial England. Chinese students go by hordes to USA. The rich Arabs have diversified to continental Europe from France to Germany to Spain. London's key banks have also been affected by recession woes and LIBOR fixing scandals and even probable legal violations (in USA) . The Pound is no more an alternative currency, forget a safe haven. Cable (GBP/Dollar) is virtually history.

With the growth of Dubai, Arab funds might see a return nearer home; with Singapore's proximity to China ; with ECB in Frankfurt, with the colonies no more to fund regal splendour; with its universities badly behind in revenues and perhaps research, with Scottish threats, imperious London's real estate and real finances may soon be under pressure.

Europe: distant footsteps of some hope

Germany's jobless fell by 14000 and markets cheered. Markets ignored that it could be a seasonal trigger or that there was a 6.6 % unemployment. Markets also discounted geo-political friction on the Russian border. Markets took lower capital investment in its stride as it clutched on to Draghi's 'talking up of inflation' and raced to buy. Industrial confidence improved although still in negative territory. Overall, buyers exceeded sellers.

Bank of Japan on effect of monetary accommodation

Hiroshi Nakaso: The potential impact of large-scale monetary

accommodation

Remarks by Mr Hiroshi Nakaso, Deputy Governor of the Bank of Japan, at the Paris

Europlace Financial Forum, Tokyo, 25 November 2014.

would inevitably boost the central bank’s presence in the financial markets

and create a resulting trade off between the intended policy consequences and the

functioning of financial markets. To minimize the potential side effects on market functioning,

the central bank should be committed to continuous dialogue with the market, so that it can

share its views on its policy intention and its outlook for the economy and inflation, as well as

accurately grasp participants’ views on market developments. The Bank of Japan has been,

and will continue to be, committed to these efforts.

http://www.bis.org/review/r141127a.pdf

Wednesday, November 26, 2014

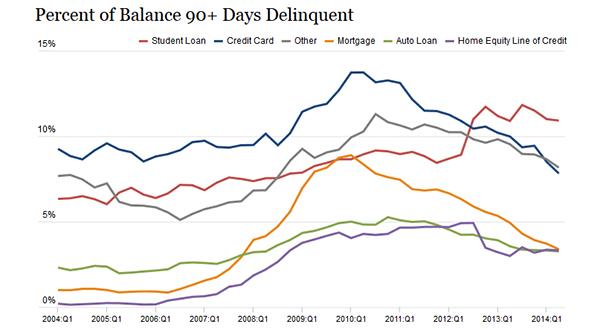

Indian banks overburdened by NPA...

Excerpt from Guv Raghuram Rajan's recent speech:

"The amount recovered from cases decided in 2013-14 under DRTs was Rs. 30590 crore while the outstanding value of debt sought to be recovered was a huge Rs. 2,36,600 crore. Thus recovery was only 13% of the amount at stake.

Worse, even though the law indicates that cases before the DRT should be disposed off in 6 months, only about a fourth of the cases pending at the beginning of the year are disposed off during the year – suggesting a four year wait even if the tribunals focus only on old cases. However, in 2013-14, the number of new cases filed during the year was about one and a half times the cases disposed off during the year. Thus backlogs and delays are growing, not coming down."

As just one measure, the total write-offs of loans made by the commercial banks in the last five years is 161018 crore, which is 1.27% of GDP. Of course, some of this amount will be recovered, but given the size of stressed assets in the system, there will be more write-offs to come.

"The amount recovered from cases decided in 2013-14 under DRTs was Rs. 30590 crore while the outstanding value of debt sought to be recovered was a huge Rs. 2,36,600 crore. Thus recovery was only 13% of the amount at stake.

Worse, even though the law indicates that cases before the DRT should be disposed off in 6 months, only about a fourth of the cases pending at the beginning of the year are disposed off during the year – suggesting a four year wait even if the tribunals focus only on old cases. However, in 2013-14, the number of new cases filed during the year was about one and a half times the cases disposed off during the year. Thus backlogs and delays are growing, not coming down."

As just one measure, the total write-offs of loans made by the commercial banks in the last five years is 161018 crore, which is 1.27% of GDP. Of course, some of this amount will be recovered, but given the size of stressed assets in the system, there will be more write-offs to come.

Valueless Managements

Goldman Sachs , HSBC, Standard Chartered and BASF managements are being sued in the US for trading in metals armed with insider client information. If true, it suggests that managements, in their yearning for profits are giving scant regard to values and ethics.

Should be another quiet market day...

With Thanksgiving on, markets have time to observe. Light on investments, heavy on absorption. With hopes pinned by retailers on Black Friday and with some interest in the OPEC meet,it is a wait by the sidelines for trends.

In India, journalists seem to suggest Prime Ministerial unhappiness with the slow approach of the Reserve Bank of India. Traditionally, RBI has been in its Mint Street ivory castle where it takes pride in some intellectual tower window. That RBI window is largely price model driven. Sitting on the 17th floor of the monetary castle, it seems oblivious of delays in decision making; of the labyrinthine knots of multiple regulatory misadventures. There is no financial supervision accountability fixed for Sahara to Sarada to 'blade mafias'. Despite such over-regulated zeal, the banking sector is under-performing.

Non-performing assets (NPAs) in the housing loan segment of public sector banks have shot up by over Rs 1,000 crore to around Rs 6,200 crore during the first six months of calendar 2014. - See more at: http://indianexpress.com/article/business/business-others/home-loan-npas-rise-by-r1000-crore-in-6-months/#sthash.bOTUsx9e.dpuf

In India, journalists seem to suggest Prime Ministerial unhappiness with the slow approach of the Reserve Bank of India. Traditionally, RBI has been in its Mint Street ivory castle where it takes pride in some intellectual tower window. That RBI window is largely price model driven. Sitting on the 17th floor of the monetary castle, it seems oblivious of delays in decision making; of the labyrinthine knots of multiple regulatory misadventures. There is no financial supervision accountability fixed for Sahara to Sarada to 'blade mafias'. Despite such over-regulated zeal, the banking sector is under-performing.

Non-performing assets (NPAs) in the housing loan segment of public sector banks have shot up by over Rs 1,000 crore to around Rs 6,200 crore during the first six months of calendar 2014. - See more at: http://indianexpress.com/article/business/business-others/home-loan-npas-rise-by-r1000-crore-in-6-months/#sthash.bOTUsx9e.dpuf

Oil on slippery ground...

OPEC just cannot be a cartel anymore. With just about 42 % of world's production share, it cannot be as influential as it used to be. OPEC is a divided house. As such, it cannot be so joined in action. Cuts of say a million barrels will be compensated by others who might want to sell off early in a falling market.

Oil prices therefore should drift south in any case even after a probable cut. Maybe good news for Asia and to the non oil companies of USA and Europe as production costs will fall. Companies like Shell and BP who have invested may see stretched bottom lines.

Oil prices therefore should drift south in any case even after a probable cut. Maybe good news for Asia and to the non oil companies of USA and Europe as production costs will fall. Companies like Shell and BP who have invested may see stretched bottom lines.

Nevertheless ECB Moves...

But in 2015.

ECB Prepared to Buy Sovereign Bonds Early 2015 , Says Constancio

Vice

President Constancio Says Central Bank to Decide in First Quarter

Good news if the Germans agree!

Brain train to USA

Deloitte Touche Global Economic Outlook 4th Quarter 2014

Deloitte Touche Ross has just released its Global Economic Outlook: It says:

United States: Back on track after first-quarter detour

Germany is losing momentum . . but its growth path remains intact

Eurozone: Recovery stalled...The recovery is still highly vulnerable to external influences.

China: Signs of continuing weakness...Despite concerns about credit market excesses, China’s central bank has chosen to ease monetary policy

Japan: Slow growth raises tax questions

India: Challenges: Manufacturing sector still unstable: High fiscal deficit; Inflation still a concern:

United States: Back on track after first-quarter detour

Germany is losing momentum . . but its growth path remains intact

Eurozone: Recovery stalled...The recovery is still highly vulnerable to external influences.

China: Signs of continuing weakness...Despite concerns about credit market excesses, China’s central bank has chosen to ease monetary policy

Japan: Slow growth raises tax questions

India: Challenges: Manufacturing sector still unstable: High fiscal deficit; Inflation still a concern:

How should governments promote exports?

Source of article: World Economic Forum

http://forumblog.org/2014/11/how-should-governments-promote-exports/?utm_content=buffer43d4c&utm_medium=social&utm_source=twitter.com&utm_campaign=buffer

Good advice on credit card

Washington Post:

How to limit your chances of fraud during the holidays

http://www.washingtonpost.com/news/get-there/wp/2014/11/26/how-to-limit-your-chances-of-fraud-during-the-holidays/?Post+generic=%3Ftid%3Dsm_twitter_washingtonpostNovember in December?

Normally, end December is quiet time in the market. Investors are away. They cut their positions for a well earned holiday.

Today's market appears to reflect that. Investors seem to wait by the sidelines. Not much action. Some inconsistent data not in sync with the usual US economy of recent days. Capital goods orders fell; jobless claims rose and anxieties rose.

When in doubt, cut positions and wait for the next big move.

Today's market appears to reflect that. Investors seem to wait by the sidelines. Not much action. Some inconsistent data not in sync with the usual US economy of recent days. Capital goods orders fell; jobless claims rose and anxieties rose.

When in doubt, cut positions and wait for the next big move.

Tuesday, November 25, 2014

China...

An article on China:

http://dupress.com/articles/asia-pacific-economic-outlook-december-2014-china/?id=gx:2sm:3tw:4dup1068:5eng:6dup:20141121212000:apac1214

China , after growing solid for nearly 35 years, is there room for concern?

http://dupress.com/articles/asia-pacific-economic-outlook-december-2014-china/?id=gx:2sm:3tw:4dup1068:5eng:6dup:20141121212000:apac1214

China , after growing solid for nearly 35 years, is there room for concern?

A hesitant consumer...

Consumer confidence in USA fell , contrary to expectations. For the forthcoming holidays, that was a shade disappointing.

That implies that consumers are not so sanguine of the future. They prefer to save rather than spend as they feel that future incomes are likely to fall. As that means a withdrawal from spending, demand takes a hit. Corporates are likely to see a miss in targets unless this hesitation is momentary. The consumer should not , hopefully, get into the Japanese mould of waiting for further falls in prices!

With oil glut, Chinese, and European and Latin American worries, markets look set for falls today. Sellers may just about seize the moment. Dollar looks hesitant as Yen, already strengthened by Aussie weakness, might gain. A day of the non-buyers.

That implies that consumers are not so sanguine of the future. They prefer to save rather than spend as they feel that future incomes are likely to fall. As that means a withdrawal from spending, demand takes a hit. Corporates are likely to see a miss in targets unless this hesitation is momentary. The consumer should not , hopefully, get into the Japanese mould of waiting for further falls in prices!

With oil glut, Chinese, and European and Latin American worries, markets look set for falls today. Sellers may just about seize the moment. Dollar looks hesitant as Yen, already strengthened by Aussie weakness, might gain. A day of the non-buyers.

Good news again:

Aggregate household debt balances increased slightly in the third quarter of 2014. As of September 30, 2014, total household indebtedness was $11.71 trillion, up by 0.7 percent from its level in the second quarter of 2014, an increase of $78 billion. Overall household debt still remains 7.6 percent below its 2008 Q3 peak of $12.68 trillion.

Source:http://www.newyorkfed.org/microeconomics/hhdc.html#/2014/q3

USA: reinforced growth...

With the accelerated GDP growth figure, Wall Street gets the right impetus. Global growth is reinforced. Markets look set for overcoming the restraint of profit taking.

RBI moves a bit...

Press Trust of India reports "RBI exploring ways to allow banks more flexibility in loan restructuring to get stalled projects on track: Governor Raghuram Rajan"

Papal Economics is Sound Advice!

Pope Francis has said that Europe is looking 'somewhat elderly and haggard' and has sought opening of Europe to immigration. (http://www.bbc.com/news/world-europe-30180667)

If Europe has to stay competitive it better listen to these words of wisdom.

Or with European economics, is wisdom a latecomer?

If Europe has to stay competitive it better listen to these words of wisdom.

Or with European economics, is wisdom a latecomer?

Wall Street encouraged...

By European optimism and the weaknesses in oil. Cost of production will be held back by both lower input costs (oil, immigrants, outsourcing, choice of techniques) and focused technological up-gradation. As USA picks up steam, there is bound to be a flow out of emerging economies in to US assets. With Brazilian and Venezuelan currencies in marked decline, there will be a flight to dollar assets and dollarization. It will impact other Latin American currencies too; and should in its sweep shake up the Asians too. Middle East markets would be affected by the nearly 30% fall in oil prices and markets like Dubai will again see pressures of sale.

Masterly inactivity by the central bank...

Can the central banks consider themselves to be apart? Can they be reluctant to listen to the Governmental or to industry pleas?Can it be that the Central bank, in its pursuit of the monetary policy, be obsessed with price management and leave growth management to non monetary interventions?

India needs 8 % but gets 5 % growth: yet the Reserve Bank of India continues in its state of ' concerned inactivity'.

India needs 8 % but gets 5 % growth: yet the Reserve Bank of India continues in its state of ' concerned inactivity'.

Monday, November 24, 2014

Rupee Weak ...

With the Dollar in to long strides, emerging currencies will be under pressure. The depreciation in the Rupee is therefore on expected lines. US assets look good to the investor. So there will be flow in to quality. Europe is still an unsure bet despite the latest German data. With Latin America on a not so certain path, investors would seek out USA. That means Rupee along with other emerging currencies should be under pressure.

Mumbai retreats...

That is quite a normal thing to happen. Markets cannot just be buyers all the time. There must be dips in the market curve and that is quite reassuring as it indicates that both buyers and sellers are active in the trade. Profits have to be booked.

Emerging markets have also to reckon with the rush in to USA too. Overall, the US and Indian markets both look good but to an experienced investor, New York appeals.

Emerging markets have also to reckon with the rush in to USA too. Overall, the US and Indian markets both look good but to an experienced investor, New York appeals.

OECD Report on India , 2014 critical of the economy...

Main findings

Improving the macroeconomic framework to support sustainable and inclusive growth.

, growth faltered between 2012 and2014 as gains from past reforms diminished, and fiscal and monetary stimuli could nolonger be sustained due to high inflation and current account deficit.

As fiscal and monetary policies have been gradually tightened, the fiscal

deficit and inflation have started to decline while the current account deficit has narrowed.

Activity has rebounded in 2014 and is projected to accelerate but the implementation of

reforms is critical. The government efforts to simplify regulations and administrative

procedures should enhance rule of law. Still-high inflation, the fiscal deficit, rising nonperforming

loans, and structural bottlenecks are also key downside risks. Large energy and

fertiliser subsidies and delays in passing key tax reforms constrain the public investment

in physical and social infrastructure, including education and health, needed for long-term

growth and lower inequalities.

Raising employment and valued added from the manufacturing sector. The

manufacturing sector could contribute more to income, export and employment growth. In

recent years, structural bottlenecks have affected the manufacturing sector more than

services. Labour and tax regulations are complex and raise cost of doing business above a

certain size. Manufacturing firms therefore tend to be small and their productivity is low.

Firms often cannot find employees with the right education and training. Frequent power

outages, difficulty in acquiring land and poor transport infrastructure also make it difficult

for firms to be competitive and reach new markets.

Increasing female economic participation. Creating more and better employment for

women has a high growth potential. Female economic participation is low, reducing

growth and living standards. Many women work in marginal jobs and have much lower pay

than men. A host of factors constrain women in the labour market, including cultural

norms, safety concerns, lack of child care and poor infrastructure. At the same time, high

unemployment among educated women, revealed preference for work in surveys, and low

net job creation point to demand problems.

Improving health outcomes for all. Health outcomes have improved substantially but

remain below countries at a similar level of development. Lack of access to a clean water

supply, nutrition deficiencies and smoking all lower health but the recent initiative on

sanitation should help. And when they fall sick, most Indians do not have access to high

quality medical services. The low level of public resources invested in health, the lack of

health care professionals, poor regulation of health services, large out-of-pocket payments

and inequality in access to health care are serious issues, in particular for the poor and

those living in rural areas and urban slums.EXECUTIVE SUMMARY

OECD ECONOMIC SURVEYS: INDIA © OECD 2014 11

Improving the macroeconomic framework to support sustainable and inclusive growth.

, growth faltered between 2012 and2014 as gains from past reforms diminished, and fiscal and monetary stimuli could nolonger be sustained due to high inflation and current account deficit.

As fiscal and monetary policies have been gradually tightened, the fiscal

deficit and inflation have started to decline while the current account deficit has narrowed.

Activity has rebounded in 2014 and is projected to accelerate but the implementation of

reforms is critical. The government efforts to simplify regulations and administrative

procedures should enhance rule of law. Still-high inflation, the fiscal deficit, rising nonperforming

loans, and structural bottlenecks are also key downside risks. Large energy and

fertiliser subsidies and delays in passing key tax reforms constrain the public investment

in physical and social infrastructure, including education and health, needed for long-term

growth and lower inequalities.

Raising employment and valued added from the manufacturing sector. The

manufacturing sector could contribute more to income, export and employment growth. In

recent years, structural bottlenecks have affected the manufacturing sector more than

services. Labour and tax regulations are complex and raise cost of doing business above a

certain size. Manufacturing firms therefore tend to be small and their productivity is low.

Firms often cannot find employees with the right education and training. Frequent power

outages, difficulty in acquiring land and poor transport infrastructure also make it difficult

for firms to be competitive and reach new markets.

Increasing female economic participation. Creating more and better employment for

women has a high growth potential. Female economic participation is low, reducing

growth and living standards. Many women work in marginal jobs and have much lower pay

than men. A host of factors constrain women in the labour market, including cultural

norms, safety concerns, lack of child care and poor infrastructure. At the same time, high

unemployment among educated women, revealed preference for work in surveys, and low

net job creation point to demand problems.

Improving health outcomes for all. Health outcomes have improved substantially but

remain below countries at a similar level of development. Lack of access to a clean water

supply, nutrition deficiencies and smoking all lower health but the recent initiative on

sanitation should help. And when they fall sick, most Indians do not have access to high

quality medical services. The low level of public resources invested in health, the lack of

health care professionals, poor regulation of health services, large out-of-pocket payments

and inequality in access to health care are serious issues, in particular for the poor and

those living in rural areas and urban slums.EXECUTIVE SUMMARY

OECD ECONOMIC SURVEYS: INDIA © OECD 2014 11

Is Brazilian Real an example for emerging currencies?

The Brazilian currency is under pressure. It has been at levels falling near 2005 levels. The pressure is on with a flight to quality to US assets. With the US recovery and its prowess in technology, there is likely to be a serious exit from emerging currencies to the US Dollar. This will start off possibly with Latam, and South East Asian assets being shed even by the wealthy nationals. With oil prices down, Indonesia and Venezuela should see serious problems.Wall Street should benefit.

On China

World Economic Forum's Analysis:

http://forumblog.org/2014/11/how-china-is-rebalancing-its-economy/?utm_content=bufferb829a&utm_medium=social&utm_source=twitter.com&utm_campaign=buffer

http://forumblog.org/2014/11/how-china-is-rebalancing-its-economy/?utm_content=bufferb829a&utm_medium=social&utm_source=twitter.com&utm_campaign=buffer

It is a monetary revival...

Central bankers are playing the role of the Keynesian norms of fiscal policy. In order not to crowd out efficiency, the monetary transmission mechanism is being used by ECB and China to route funding to the private sector. That moves the overall efficiency curve to the right. so that capital output ratio is optimized.

It looks like growth is here to stay for some time. Employment should expand.

It looks like growth is here to stay for some time. Employment should expand.

QE becomes global...

Looks like China and Europe are drawing leaves from the Fed. The markets seem to cheer the news by rollicking high...

Gold and oil might move up too with the dollar...

Gold and oil might move up too with the dollar...

Retail investor, read on...

Some quotes which worry me:

Source 1 : Quote 1:

http://www.bloomberg.com/news/2014-11-24/draghi-urgency-for-ecb-action-gets-final-reality-check-with-data.html

"The

ECB president also explicitly cited government bond buying as a policy tool

earlier last week. “Unconventional measures might entail the purchase of a

variety of assets, one of which is sovereign bonds,” he said in Brussels Nov.

17.

The

next day, Dutch central bank chief Klaas Knot said that he is “rather

skeptical” of QE. Bundesbank President Jens Weidmann and ECB Executive Board

member Sabine Lautenschlaeger, a former Bundesbank official, are among other

policy makers who have signaled opposition to such a move.

ECB

Vice President Vitor Constancio, speaking in Florence on Nov.

22, suggested officials are in no rush to act immediately as existing measures

start to take effect."

Source 2 : Quote 2:

2. Read more at:

http://economictimes.indiatimes.com/articleshow/45256269.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

http://economictimes.indiatimes.com/articleshow/45256269.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

The Indian markets have rallied over 33 per cent

so far in the year 2014, but analysts at top investment firms are of the view

that the rally is not over yet and there is further headroom for the markets to

inch higher from the current levels.

Sunday, November 23, 2014

Rupee's Movement up ... sustainable?

The Indian Rupee has been moving up today in the initial rounds; the market is expecting inflows, perhaps. The inflows appear to be swayed by rise in the India equity market which is at levels previously untouched. Consequentially, inflows of some 'hot money' chasing high return in emerging markets would pass through India too.

One moot point is by afternoon, would the foreign investors decide to invest in their home markets even as they pick up?

One moot point is by afternoon, would the foreign investors decide to invest in their home markets even as they pick up?

Is Mumbai Stock Exchange sentiment driven?

While likelihood of Asian and European stimuli by respective central banks seem to trigger buying in international markets; protracted lingering of positive sentiment seems to differentiate the Mumbai Stock Exchange. The bidding up of the market is yet to be followed up by real economics or concrete reforms. Can a financial market survive merely on positive sentiments?

For a smart trader, may be a time to book profits?

For a smart trader, may be a time to book profits?

Merger of banks in India ...sell on the fact...

The recent Kotak Mahindra with ING Vysya Bank merger leaves some questions which nag:

a) Kotak has stated that there would be no ' drastic ' job buts. Then where are the economic synergies? Productivity is all that matters.

b) What about the cultural fusion issue: a drag on all normal HR issues?

c) While the GOI is keen to bring in foreign investment, why is a Dutch group dis-investing?

d) Is it that the foreign investors have realized the ING Vysya has assets that it needs to pass on? If that is so is the proud new bank holding a hot potato?

e) Is the banking sector not so good in the foreign investor's eyes?

Dictum in trading: Buy on the rumor, sell on the fact!!!

a) Kotak has stated that there would be no ' drastic ' job buts. Then where are the economic synergies? Productivity is all that matters.

b) What about the cultural fusion issue: a drag on all normal HR issues?

c) While the GOI is keen to bring in foreign investment, why is a Dutch group dis-investing?

d) Is it that the foreign investors have realized the ING Vysya has assets that it needs to pass on? If that is so is the proud new bank holding a hot potato?

e) Is the banking sector not so good in the foreign investor's eyes?

Dictum in trading: Buy on the rumor, sell on the fact!!!

Gold, China and Euro

With the Chinese and Euro talk and moves towards further stimulus to avoid deflation, gold seemed set to strengthen. The People’s Bank of China cut the one-year benchmark lending rate by 40 basis points to 5.6% and the one-year deposit rate by 25 basis points to 2.75%. This is expected to accelerate Chinese growth and thus shore up gold. The submission here is that it can only be technical buying and not sustained buying as

a) deflation is the global worry, not inflation;

b) China might yet take time to restore its high growth rate;

c) India has introduced Kisan Vikas Patra bonds which will see unaccounted money flow in to that route and not so much in to gold;

d) oil prices are weak and oil sellers would hesitate to invest in gold for some time yet;

e) Swiss referendum looks set to be not so benign for gold;

f) Russian buying at this point looks more geo-political rather than pure economics.

It may be a good idea for the day to sell and buy.

Friday, November 21, 2014

The Internet of Things: Affecting Business Positively

Interesting articles/ links

1. How Will the Internet of Things Affect Your Business? by

John Rampton

http://www.forbes.com/sites/johnrampton/2014/11/21/how-will-the-internet-of-things-affect-your-business/

2. According to McKinsey Global Institute, the

Internet of Things has the potential to create an economic impact of $2.7

trillion to $6.2 trillion annually by 2025 (McKinsey Global Institute,

Disruptive technologies: Advances that will transform life, business, and the

global economy, May 2013).

3. http://www.microsoft.com/windowsembedded/en-us/internet-of-things.aspx

4, http://www.microsoft.com/windowsembedded/en-us/internet-of-things-infographic.aspx#whitepaper

RBI: conceiving but not delivering?

“Recalling his initial days as a Prime Minister, Modi said when he asked how much time RBI would take to open bank accounts for 7.5 crore families who are out of the banking net, the central bank had told him it would take three years.

I asked the RBI, this work has to be done. RBI said, it could be done…as no one can dare refuse Prime Minister…but they know the techniques. They said it would take three years,” (Prime Minister Modi)

http://www.financialexpress.com/article/economy/narendra-modi-does-a-first-takes-a-dig-at-guv-raghuram-rajan-led-rbi/

RBI perhaps needs to rethink itself. A good beginning may be a holiday for RBI seniors' speeches and conferences; and possibly a cut loss approach to meetings; devoting gained time to rethink on how we can meaningfully work towards inclusion.

According to a search on RBI's website for speeches there were 70 speeches between February 7 2012 and October 14, 2014 which had the words financial inclusion in them.

http://rbi.org.in/searchnew/scripts/SearchResults.aspx?search=financial+inclusion&ordby=date&Cond=2&Fromd=0&Tod=0&Archives=0&SecName=Speeches

A search on 'Jan Dhan Yojana' did not throw up any results.

No wonder why the PM is a shade upset.

I asked the RBI, this work has to be done. RBI said, it could be done…as no one can dare refuse Prime Minister…but they know the techniques. They said it would take three years,” (Prime Minister Modi)

http://www.financialexpress.com/article/economy/narendra-modi-does-a-first-takes-a-dig-at-guv-raghuram-rajan-led-rbi/

RBI perhaps needs to rethink itself. A good beginning may be a holiday for RBI seniors' speeches and conferences; and possibly a cut loss approach to meetings; devoting gained time to rethink on how we can meaningfully work towards inclusion.

According to a search on RBI's website for speeches there were 70 speeches between February 7 2012 and October 14, 2014 which had the words financial inclusion in them.

http://rbi.org.in/searchnew/scripts/SearchResults.aspx?search=financial+inclusion&ordby=date&Cond=2&Fromd=0&Tod=0&Archives=0&SecName=Speeches

A search on 'Jan Dhan Yojana' did not throw up any results.

No wonder why the PM is a shade upset.

Draghi seeks support...

Draghi needs support. Germany are you listening? On previous occasions, Germany has disregarded sane pleas on crucial occasions : recall 1992 Deutsche Mark ; British pound and French franc cases. Markets hope that Germany will not play spoil sport this time. Fears of deflation in Europe should prod Germany . . . Or will they force lonely trudge on Draghi? Thank the US regulators for pulling out the US Economy!

Thursday, November 20, 2014

USA and immigration

The single biggest contributor to America is the American dream. Immigration helps keep the wages in check. There is a flow of able bodied and willing entrepurial worker who keeps chasing the dream.That ticks off the US Economy. European thinking is relatively closed. So economies that are open to wage inflows have prospered. Bet on the US industry which has creativity and youth.

UK buys furniture...

October data released shows that consumer spending was good in October (+0.8 on the month) with the UK inhabitants buying more of furniture. In UK, people seem inclined to spending despite a weak Europe who are not inclined to import. A weak pound should help exports. Overall it looks positive for global recovery. USA and UK would normally seem to have correlation on the upswing. Thatcher was right in keeping London out of Euro.

Weaknesses of Europe and China already factored in...

China's weaknesses and a weak Europe are factors already factored in. Then why should traders sell on this news? The US economy is emerging stronger with benign housing data. So Wall Street may see inflows and thus higher levels. The appreciation in the dollar is indicative.

Wednesday, November 19, 2014

Strategic re-invention of the US economy...

Falling oil prices is good news for all except oil producers.

The United States has quietly re-positioned itself. It has become a great geo-strategic force once again on the back of its technology and its oil reserves. Iran earlier and now Russia are realizing that the world can do without its oil.

Soon enough, Saudi Arabia which is trying to hold on to its market share will realize that it is committing price harakiri.

Its discriminatory pricing strategy will adversely affect it; selling cheaper to America at the cost of Asia will leave it with few buyers in the long run. Dubai will feel the impact of slowing growth if oil producers slow down.

If India carries its efforts at bringing money stashed away abroad, just as USA has been doing, there will be quite a few money centres and real estate prices shaken up gradually, if not suddenly.

The United States has quietly re-positioned itself. It has become a great geo-strategic force once again on the back of its technology and its oil reserves. Iran earlier and now Russia are realizing that the world can do without its oil.

Soon enough, Saudi Arabia which is trying to hold on to its market share will realize that it is committing price harakiri.

Its discriminatory pricing strategy will adversely affect it; selling cheaper to America at the cost of Asia will leave it with few buyers in the long run. Dubai will feel the impact of slowing growth if oil producers slow down.

If India carries its efforts at bringing money stashed away abroad, just as USA has been doing, there will be quite a few money centres and real estate prices shaken up gradually, if not suddenly.

China PMI shows slowdown...

http://www.business-standard.com/article/reuters/china-nov-flash-hsbc-pmi-falls-to-50-0-output-shrinks-for-first-time-in-6-months-114112000092_1.html

Gold - Short Sell tactic

1. Given that the Fed has some voices suggesting a trend towards falling prices, gold has lost its 'hedge role' charm. There is little on the political front or economic news to support the metal.

2. The slide in oil prices is expected to adversely impact gold as oil suppliers are also normally buyers of the metal. China is quiet and the Indian consumer is waiting for falling prices.

3. The non banking finance industry will be under strain as safety margins erode and would ask borrowers to withdraw or face auction. In any case there is a supply move.

4. With the Swiss referendum showing a move away from gold, short selling may be the trader's tactic for the day.

2. The slide in oil prices is expected to adversely impact gold as oil suppliers are also normally buyers of the metal. China is quiet and the Indian consumer is waiting for falling prices.

3. The non banking finance industry will be under strain as safety margins erode and would ask borrowers to withdraw or face auction. In any case there is a supply move.

4. With the Swiss referendum showing a move away from gold, short selling may be the trader's tactic for the day.

Sagacious Fed...

Apprehensive of a potential slide back to recessionary trend, the Fed took a cautious stance. This has done and is doing the global recovery good. This bid of anxiety at possibility of deflation rearing its head is real, given the experience of Japan and Europe. So the Fed has tread rather circumspectly and balanced well.

All in all, the news is benign for emerging economies like India. FIIs might stay a little longer here. With Yen weakening Asia should be more optimistic than it appears to be. May be Chinese concerns worry a bit but the market has already discounted that.

With US dollar strengthening and less of fear of inflation, gold will continue to recede...

A day of in and out trading; not much of a position to hold. Buy on the trend sell at the best seen...

All in all, the news is benign for emerging economies like India. FIIs might stay a little longer here. With Yen weakening Asia should be more optimistic than it appears to be. May be Chinese concerns worry a bit but the market has already discounted that.

With US dollar strengthening and less of fear of inflation, gold will continue to recede...

A day of in and out trading; not much of a position to hold. Buy on the trend sell at the best seen...

Swiss as a destination of safety

However much the Swiss National Bank tries to stem the inflow, there is little escape from the investor perception of Swiss assets as a safe destination for investment. So the Swiss index has been rising. European shares have also been rising but yet some investors choose Swiss over other European assets. Some countries continue to attract.

Oil prices...

Blizzard conditions are chillingly sad...

As winter hurts, oil may see some demand ...

As winter hurts, oil may see some demand ...

Permits at 6.5 year high; but housing starts decline

http://www.reuters.com/article/2014/11/19/us-economy-housingstarts-idUSKCN0J31DZ20141119?feedType=RSS&feedName=businessNews

Interpretation: No change in outlook which is positive.

Interpretation: No change in outlook which is positive.

The Internet of Things will drive a bull market.

- Abeonomics is on despite temporary setbacks;

- US economy is throwing out the right signals: just enough to keep interest rates high and just right to have no worries on prices;

- Europe's Central Bank seems to assimilate the benign effect of QE;

- China will grow , continue to grow and will lead in growth figures despite all its slow down worries;

- Indian reforms are back on track; although India is far behind China, it is seriously for once, trying to make a dash for it;

- Technology is helping corporates with enhanced productivity.

- The Internet of Things will keep on lifting the markets...

Tuesday, November 18, 2014

Do Indians overbuy?

Indian Stock markets are touching previously unseen heights. Optimism is fueled by Great expectations on reforms being rolled out.

With the 150 plus million middle class and with PM Modi determined to mobilise the rural areas too, it looks all set to grow. India is trying to give a push to infrastructure too.

Given that the Reserve Bank, in typical Bundesbank style seems obseesed with inflation, corporates still await softer interest rates. FIIs may also disinvest for USA as that economy looks better. So the best advice seems to be ride the trend of the market but exit before the others. Do not fall in love with your investments.

With the 150 plus million middle class and with PM Modi determined to mobilise the rural areas too, it looks all set to grow. India is trying to give a push to infrastructure too.

Given that the Reserve Bank, in typical Bundesbank style seems obseesed with inflation, corporates still await softer interest rates. FIIs may also disinvest for USA as that economy looks better. So the best advice seems to be ride the trend of the market but exit before the others. Do not fall in love with your investments.

Looks set for a buyer's day?

Global Equity markets are as optimistic as one can be in the given circumstances:

a) Japan is going to polls;

b) Bank of Japan has to expand money supply;

c) Japan has to delay taxing, which means real incomes are better off;

d) India looks for a strong reform agenda;

f) Oil prices look set south further;

g) Dollar is rising showing inward flows in to USA;

h) With dollar's rise middle east economies outward buying is enhanced so the European and Asian suppliers are likely to benefit.

Dollar high; gold slipping further;

Emerging markets, will they see a rush to the Wall Street?

a) Japan is going to polls;

b) Bank of Japan has to expand money supply;

c) Japan has to delay taxing, which means real incomes are better off;

d) India looks for a strong reform agenda;

f) Oil prices look set south further;

g) Dollar is rising showing inward flows in to USA;

h) With dollar's rise middle east economies outward buying is enhanced so the European and Asian suppliers are likely to benefit.

Dollar high; gold slipping further;

Emerging markets, will they see a rush to the Wall Street?

India seeks Uranium for driving growth...

"The (Australian )uranium industry is hoping to make trial shipments to India next year as the nation (India) makes plans to move to 25 per cent nuclear power by 2050.

Prime Minister Tony Abbott and Indian leader Narendra Modi have discussed the supply of Australian uranium for India's nuclear power plants."

"There are currently 435

operable civil nuclear power nuclear reactors around

the world, with a further 71

under construction..

Nuclear energy is used to generate

around 11% of the world's electricity, with almost no greenhouse gas emissions.

Nuclear energy is used by more than

30 countries around the world. Nuclear technologies have many uses, including

powering Mars rovers.

Percentage share

|

Electricity Supplied TWh

|

|

Argentina

|

5

|

5.9

|

Armenia

|

33.2

|

2.4

|

Belgium

|

54

|

45.9

|

Brazil

|

3.2

|

14.8

|

Bulgaria

|

32.6

|

15.3

|

Canada

|

15.3

|

88.3

|

China Mainland

|

1.8

|

82.6

|

Czech Rep

|

33

|

26.7

|

Finland

|

31.6

|

31.6

|

France

|

77.7

|

423.5

|

Germany

|

17.8

|

102.3

|

Hungary

|

43.2

|

14.7

|

India

|

3.7

|

28.9

|

Japan

|

18.1

|

156.2

|

Mexico

|

3.6

|

9.3

|

Netherlands

|

3.6

|

3.9

|

Pakistan

|

3.8

|

3.8

|

Romania

|

19

|

10.8

|

Russia

|

17.6

|

162.0

|

Slovakia

|

54

|

14.3

|

Slovenia

|

41.7

|

5.9

|

South Africa

|

5.2

|

12.9

|

South Korea

|

34.6

|

147.8

|

Spain

|

19.5

|

55.1

|

Sweden

|

39.6

|

58.1

|

Switzerland

|

40.8

|

25.7

|

Taiwan

|

19

|

40.4

|

UK

|

17.8

|

62.7

|

Ukraine

|

47.2

|

84.9

|

USA

|

19.2

|

790.4

|

"

Source : http://www.world-nuclear.org/Nuclear-Basics/Electricity-supplied-by-nuclear-energy/

Uranium prices to advance?

Uranium prices have been rising :

Uranium Oxide Price 41.75 USD/lb

52 Week Low 28.00 USD/lb 52 Week High 41.75 USD/lb

Great revival

Abeonomics is back in focus as Japan goes to polls again. Will the ruling party win with the writ and vigor to carry forward? In any case, markets cannot be worried, because Japan cannot get any worse. In fact QE seems inevitable.

US producer inflation is indicative of a great revival after the great recession. With ECB too looking to QE the world looks stimulus led growth for the great revival. .,

US producer inflation is indicative of a great revival after the great recession. With ECB too looking to QE the world looks stimulus led growth for the great revival. .,

Of Merger Mania...

Wall Street is excited about the latest news from merger front. It appears to be a good case that shareholders must buy on the rumour and sell on the fact. Merger economics may not be so benign in the long run. With oil prices declining, extraction costs may be higher and ancillary services may suffer adversity.

Gold between glimmer and glitter

1. Gold referendum of Swiss National Bank " 30 November 2014

If there is a yes vote ( which will mean that SNB has to buy gold) then SNB may stagger purchases. The impact of an SNB purchase (if at all there is a yes vote) may not be so impacting on the gold prices.

http://www.reuters.com/article/2014/11/17/swiss-gold-referendum-idUSL6N0T72O620141117

2. ECB might set out on quantitative easing a la the Fed. However, inflation has not reared its head and so gold may not be so much needed as a hedge.

3. Japanese have decided to restart 2 nuclear reactors and hence price of uranium has started to move up. So precious metal investors have another market to buy.

If there is a yes vote ( which will mean that SNB has to buy gold) then SNB may stagger purchases. The impact of an SNB purchase (if at all there is a yes vote) may not be so impacting on the gold prices.

http://www.reuters.com/article/2014/11/17/swiss-gold-referendum-idUSL6N0T72O620141117

2. ECB might set out on quantitative easing a la the Fed. However, inflation has not reared its head and so gold may not be so much needed as a hedge.

3. Japanese have decided to restart 2 nuclear reactors and hence price of uranium has started to move up. So precious metal investors have another market to buy.

Bull run expectation reinforced.

Abenomics should see Japan through. Efforts are on to weaken the yen, revive profits and help restore confidence in the economy. There are blips like the technicality of recession; but then the Japanese economy has been on a 'price harakiri' since 1990s. Price falls have hollowed out Japanese manufacturing.

So stimulus has to be on: we really are looking at softer interest rates for quite a few months from now on. So Gold is again picking up. The strengthening of the Euro , is however a cause for concern for the Europeans. US economy would benefit and hence Wall Street should do well.

So stimulus has to be on: we really are looking at softer interest rates for quite a few months from now on. So Gold is again picking up. The strengthening of the Euro , is however a cause for concern for the Europeans. US economy would benefit and hence Wall Street should do well.

Monday, November 17, 2014

Indian stocks look good today

With SBI being on a NPA recovery path, financial stocks are likely to push Indian stock higher today. Among Emerging economies India looks most promising and so foreigners seem to park at least till there are alternatives. All set , it looks , like a high day. With Australia balancing well between India and China, it seems a buy day.

http://in.reuters.com/article/2014/11/17/australia-india-trade-idINKCN0J12DX20141117

http://in.reuters.com/article/2014/11/17/australia-india-trade-idINKCN0J12DX20141117

Japan rebound and Swiss Vote...

Japan is putting an act together to support 'Abenomics'. The Japanese seem to return to the markets. Australia and China have entered a trade deal. There is greater access to the Chinese capital markets. The Indian PM is also meeting the Ozzie PM ; and Indian banks have given $ 1 billion to the Adani Group for their coal mining in Australia.

All positives for growth.

The Swiss, in typical European manner have voted against immigration and that should indicate a negative point for Europe. Europe is still living in the past and we hope are not frozen in the past.Asia and Americas are realistic and thus growth will bypass the Europeans. The euro has been rather high and is a millstone round a faltering economy. Unless the Europeans change their approach to the economics of immigration, they may be left behind as costing (high wage europeans) and ageing (older demographic structure) will push them back . ECB is in its state of inertia

The US Dollar is doing well buoyed by the economy and gold will be pushed down in the struggle.

Mumbai looks good but one has to discount for exaggerated expectations. Wall street is on quite sober growth expectations.

Anticipation for today:

Dollar higher; Asian and American Equities higher; gold and bonds lower.

All positives for growth.

The Swiss, in typical European manner have voted against immigration and that should indicate a negative point for Europe. Europe is still living in the past and we hope are not frozen in the past.Asia and Americas are realistic and thus growth will bypass the Europeans. The euro has been rather high and is a millstone round a faltering economy. Unless the Europeans change their approach to the economics of immigration, they may be left behind as costing (high wage europeans) and ageing (older demographic structure) will push them back . ECB is in its state of inertia

The US Dollar is doing well buoyed by the economy and gold will be pushed down in the struggle.

Mumbai looks good but one has to discount for exaggerated expectations. Wall street is on quite sober growth expectations.

Anticipation for today:

Dollar higher; Asian and American Equities higher; gold and bonds lower.

Wall Street may shrug off...

The Japanese recession. Japan has been struggling for some time. That would have been factored in.So by the time the Japanese recession reaches Wall Street it may be just ripples. Germany the largest economy in Europe and France the other important economy, are doing well. So the sentiment looks likely to turn positive by New York time...

Sunday, November 16, 2014

India looking good...

Destination India...

India is a growth story that looks good if not as yet great.

Investment has to come:

India is a growth story that looks good if not as yet great.

Investment has to come:

Infrastructure needs are massive.

Only 20 percent of the national highway network is four-lane.

India's ports and airports need substantial improvement and thus investment. So multiplier will be high.

Trains are rather of another era.

It would need rapid modernization. Investment here is vital.

Rural roads need improvement. It would have multiplier effects.

An estimated 300 million people

are not connected to the national electrical grid. Infrastructure investment need is thus substantial.

The number of urban centers has

grown from about 5,000 in 2001 to 8,000 in 2011, and 53 cities already have a

population in excess of one million.

There is a need to accommodate an

additional 10 million urban dwellers every year and to provide them with

adequate basic services. This needs quite a strong of investment.

The ambitious Government programme

for financial inclusion will mop up liquidity and also enhance credit

deployment levels. It also touches on insurance comfort zone. This will promote

human development and strengthen social fabric.

India has been free of polio for nearly three years

now. Life expectancy has more than doubled from 31 years in 1947 to 65 years in

2012. Adult literacy more than quadrupled from 18 percent in 1951

to 74 percent in 2011.

In the last decade, India grew

faster than 92 percent of the world’s nations. Real GDP expanded at an average

annual rate of 7.3 percent between FY2003 and FY2012.

India is an important player in

the global information-technology revolution,

At market exchange rates, its share

of world GDP has increased by 50 percent in 30 years from 1.8 to 2.7

percent; is expected to reach 11 percent by 2050.

( Data from a World Bank on line Publication)

Japan in recession and Chinese NPA...

Asia looks south with 2 alarm bells: Japan is in technical recession with declines in 2 successive quarters and then the Chinese banks have NPAs which are worrying. Both are not new stories as both economies have been under investor observation for quite some time now.

Yen gave way and possibly the uncertainty in Europe saw a parking slot in the Aussie dollar.

Markets will be hesitant and worried investors will try to leave rather than flee. There is an orderly exit that may occur. Waiting for reassurances from policy makers.

Staying on the sidelines, may be a good trading tactic. Not a day to enter, Towards evening, when the US markets open , as the US economy is on a strong wicket, Wall Street may shrug off the data of the morning and may be Wall Street will stem the ebb.

Until then, it looks like number of sellers are more than buyers.

Yen gave way and possibly the uncertainty in Europe saw a parking slot in the Aussie dollar.

Markets will be hesitant and worried investors will try to leave rather than flee. There is an orderly exit that may occur. Waiting for reassurances from policy makers.

Staying on the sidelines, may be a good trading tactic. Not a day to enter, Towards evening, when the US markets open , as the US economy is on a strong wicket, Wall Street may shrug off the data of the morning and may be Wall Street will stem the ebb.

Until then, it looks like number of sellers are more than buyers.

Subscribe to:

Comments (Atom)